Relevant Range

In cost behavior analysis, relevant range represents the production bracket expressed in terms of units within which fixed costs are indeed fixed.

We define fixed costs as costs which do not change with increase or decrease in the number of units produced. However, this proposition is not valid indefinitely, i.e. fixed costs remain fixed only when production remains within certain minimum and maximum limit. Such limits constitute relevant range.

Identification of relevant range is important because knowing the production level at which costs will change is critical for cost accounting, budgeting and financial planning.

Example

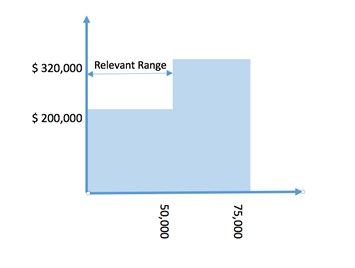

125H is a motor bike manufacturer. It stores ready-to-sell motorbikes in a rented warehouse which is designed to accommodate 50,000 units at one time. The warehouse rent per annum is $200,000 regardless of the number of bikes parked there; hence, it is a fixed cost.

During the financial year 2015, sales dropped despite sustained production which resulted in increase in number of motorbikes to be parked in the warehouse. Ending inventory as at 31 March 2015 climbed to 60,000 bikes. 125H was forced to rent out another warehouse that could accommodate 25,000 units at time for $120,000 per annum.

The increased warehouse rent will remain fixed until the maximum capacity of that second warehouse is reached i.e. inventory balance exceeds 75,000 motorbikes.

Graph

The following graphs explains the concept of relevant range. X-axis plots the number of units while Y-axis shows cost.

by Obaidullah Jan, ACA, CFA and last modified on